Your regulator does not care that the demo worked in 14 days if customer voice data leaves the environment it was supposed to stay inside. For SEA (Southeast Asia) insurers and banks, insurance call center automation fails the moment deployment is treated as an afterthought. The mistake most teams make is testing voice quality, intent handling, and containment before asking the harder infrastructure question. Can the same system run on-prem, speak the local language clearly, and hand off to a human without making the customer start over?

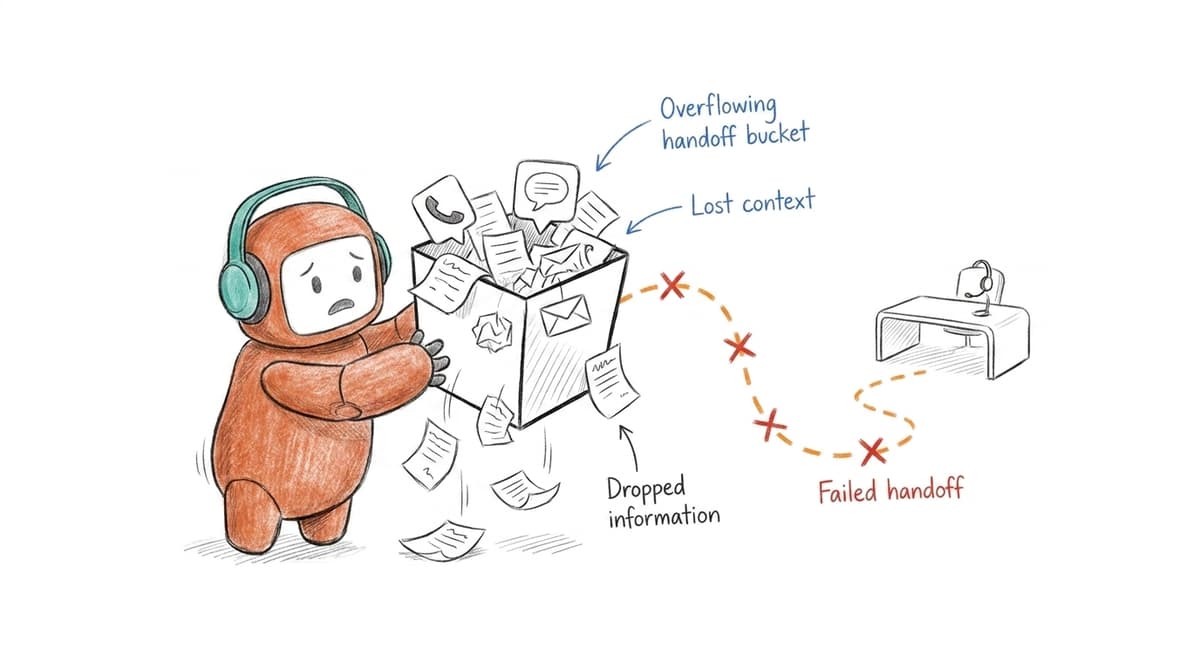

A policyholder calls about a claim. The voice vendor captures the call, the helpdesk opens a ticket, the CRM owns the policy record, the outbound dialer runs renewal calls, and the compliance report comes from somewhere else tomorrow. The customer only sees one insurer. Internally, your team is carrying a stack that was never built to act like one system.

For SEA BFSI (Banking, Financial Services, and Insurance) teams, the problem gets sharper. Cloud-only automation can be blocked by data residency rules. Generic English voice models sound wrong in Vietnamese, Thai, Bahasa, or local-accented English. And for a CTO or CIO, a vendor that cannot explain deployment, auditability, and handoff logic is not a vendor. It is risk.

Key Takeaways:

- Insurance call center automation fails when voice, chat, CRM, compliance, and outbound live in separate systems.

- Regulated insurers should decide deployment model before vendor selection, not after the pilot.

- If a call workflow crosses more than 3 tools before resolution, automation will inherit the fragmentation.

- Local-language voice quality is a technical requirement in SEA BFSI, not a customer experience add-on.

- Outbound collections, renewals, and claim follow-up belong inside customer operations, not in a separate sales tool.

- Human handoff is the safety mechanism. Automation without full context transfer creates rework and compliance exposure.

Why Insurance Call Center Automation Fails in BFSI

The call is not the workflow

Reduce repetitive inbound calls. That is usually the first automation target a call center leader picks, and the instinct is fair. Password resets, claim status checks, payment reminders, and policy questions eat agent time every day. The mistake is treating those calls as isolated events instead of parts of a regulated customer record.

Picture a CIO at a Vietnamese life insurer opening Salesforce at 8:14 AM Monday after a weekend escalation. A policyholder called Friday about a delayed claim, pinged the Zalo channel Saturday, and got an outbound payment reminder from the Genesys dialer Sunday morning. The voice transcript sits in one vendor portal. The Zalo thread sits in a separate inbox. The dialer log lives somewhere only the collections team can see. The customer has now told the same story three times to three different agents, and compliance is asking why the renewal call went out while the claim was open. That is not a voice problem. That is an architecture problem.

Before approving any insurance voice automation, walk the workflow after the first answer. If the call creates a ticket, updates a CRM, sends an SMS, triggers a compliance log, or routes to a human, those steps need one operating path. Three or more tool crossings before resolution is the warning line. Past that, automation will answer faster and resolve slower.

Point tools create hidden compliance debt

A fragmented insurance stack usually looks reasonable in procurement. One vendor for voice. One for chat. One for ticketing. One for outbound. One BI layer to make sense of it later. Each tool has a clean contract and a narrow job, so the stack feels manageable until an auditor asks who approved which message, when, and under what customer consent record.

Regulated teams do not just need call recordings. They need evidence of consent, call timing, opt-out handling, escalation decisions, script control, and customer history. The NAIC Insurance Data Security Model Law shows the direction of travel: insurers are expected to govern information security with documented controls, not loose operational memory. Different SEA markets will apply different rules, but the operating burden is similar.

A simple threshold works here. If your call center automation requires compliance staff to reconcile logs from more than 2 systems after the fact, the design is already too brittle. The safer pattern is to put policy checks and approval paths before the customer interaction, then preserve the decision trail inside the same workflow. Build the audit trail at runtime, or build it from spreadsheets at 2 AM the night before the regulator visit.

The Real Risk Is Fragmented Control

The deeper risk in insurance call center automation is not automation error. It is fragmented control over knowledge, routing, deployment, and human escalation. When those controls live in different places, the CTO inherits operational risk that no model upgrade can fix.

Cloud-only is a blocker in regulated markets

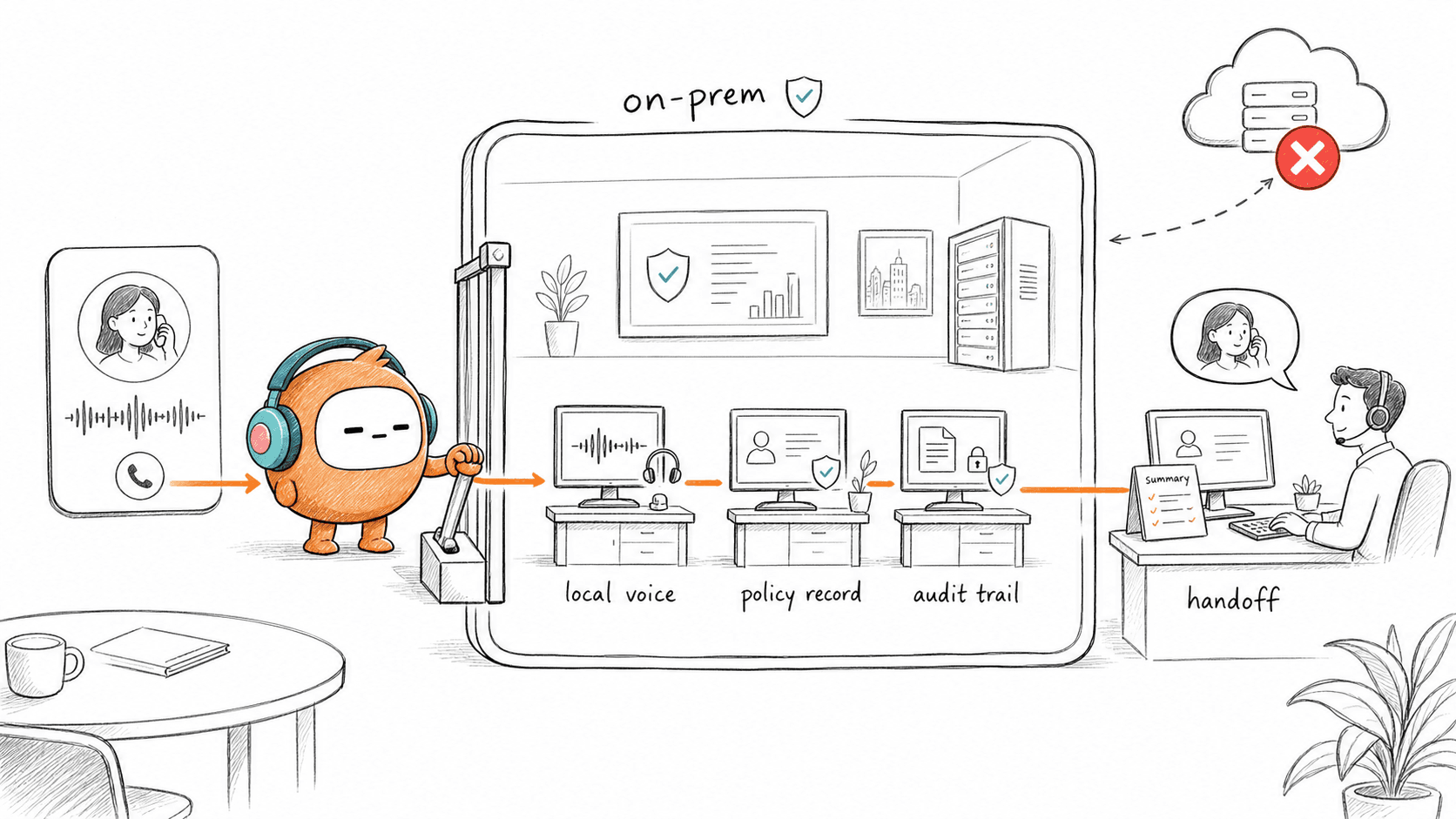

Cloud is a perfectly valid deployment path for many insurers. It is faster to start, easier to maintain, and often enough for lower-risk workloads. I would not argue against cloud as a default for every company. That would be lazy.

SEA BFSI is different. For banks, insurers, and lenders handling sensitive customer data, on-premise deployment may be the only path that passes internal governance or regulator review. In Vietnam, teams reviewing AI voice deployments should align their data handling with Law 91/2025/QH15 and the implementing rules before making public claims about compliance. The safe question is not "Can the vendor run AI?" It is "Where does the data sit, who controls the infrastructure, and what evidence can we show?"

Use a hard filter before any demo. If the workload includes regulated voice calls, local-language customer data, or outbound collections, ask for cloud and on-prem options in the first meeting. If the vendor cannot support the required model, stop the evaluation early. Three weeks of pilot excitement will not fix a deployment model your security team rejects.

Voice quality is part of the security review

Most teams separate voice quality from technology approval. CX owns the voice. IT owns the infrastructure. Legal owns the risk. In insurance, that split is artificial. A bad local-language voice creates more escalations, more repeated identity checks, and more manual intervention. Each retry adds another data event.

Vietnamese-language insurance calls are a good test case. A generic voice model may read the words correctly and still fail the conversation. Names, policy terms, regional accents, and emotional tone matter. A claim call is not a food delivery update. A payment reminder is not a marketing message. The wrong voice makes the customer suspicious before the workflow even begins.

The diagnostic is simple. Test 50 real call transcripts before launch, not 5 polished scripts. Include claims, renewals, payment reminders, complaints, and edge cases with mixed language. If more than 10% of calls require a human only because the voice sounds unnatural or misunderstands local phrasing, the automation is not production-ready.

What Broken Call Workflows Cost Insurers

Broken call workflows cost insurers time, trust, and audit confidence. The cost is not always visible in one dashboard because the loss spreads across agents, supervisors, compliance teams, and customers. That is why fragmented automation often looks fine in the pilot and fails in production.

Every handoff adds minutes and risk

A single handoff can look harmless. The AI answers, then a human agent takes over. Normal. The cost appears when the agent has to ask the customer for the same policy number, the same claim ID, and the same explanation because the handoff carried no usable context.

IBM's Cost of a Data Breach Report keeps showing the same broad lesson for regulated companies: exposure is expensive because remediation touches legal, operations, customer trust, and technical cleanup. Insurance call center automation does not need a breach to create cost. A missing consent log, a wrong message window, or a scattered transcript can still trigger weeks of review.

A practical benchmark: if an escalated call takes more than 90 seconds before the human agent understands what the AI already handled, the handoff is broken. If that happens across thousands of conversations per week, the cost becomes agent capacity, queue time, and customer patience. Small delay. Big waste.

Outbound is not a separate category

Insurance teams often treat outbound as a sales or collections tool. In my view, that is the wrong split. Renewal reminders, missed payment calls, claim follow-ups, document collection, and quote follow-up are customer operations workloads. They use the same customer identity, the same compliance rules, and the same need for conversation history.

The damage comes from separating inbound and outbound. A customer calls about a claim in the morning and receives an automated premium reminder in the afternoon. Nobody checked the open issue. Nobody paused the sequence. The policyholder hears the insurer asking for money before resolving the service problem. That is how automation loses trust.

Put outbound through the same operating test as inbound:

- Does the workflow check the customer's current status before contact?

- Does it respect local time windows, consent, and opt-out rules?

- Does it stop when a human takes ownership?

- Does it write outcomes back to the customer record?

- Does the next agent see the full sequence?

If the answer is no to any of those, outbound should not sit in a separate dialer. It belongs in the same customer operations layer as support.

How To Build Call Automation Regulators Can Approve

Call automation regulators can approve starts with control design, not model selection. The right sequence is deployment model, knowledge control, workflow ownership, escalation logic, then channel expansion. That order feels slower at first, but it prevents rework after security review.

Start with the deployment decision

The first technical decision should be where the system runs. Not the voice. Not the script. Not the agent persona. For SEA insurers, deployment is the gate that determines whether the project can move beyond slides.

Use 3 buckets. Low-risk public information workflows can usually start in cloud. Sensitive customer workflows need a formal data residency review. Regulated production voice, especially in banking, insurance, lending, or collections, may require on-premise infrastructure. The last bucket needs GPU planning, network review, failover thinking, and security involvement from day one.

There is a tradeoff. On-premise deployment gives more infrastructure control, but it asks more from IT. Cloud gets moving faster, and it may not pass policy for sensitive workloads. That is a real limitation, not a footnote. The point is to make the tradeoff explicit before vendor selection, because deployment mismatch is one of the most expensive ways to fail late.

Make knowledge boring and controlled

Insurance automation should not improvise. It should answer from approved policy wording, claims rules, payment processes, FAQ content, and escalation boundaries. A model that sounds confident outside approved knowledge is not smart. It is dangerous.

Think of the knowledge base the way a pharmacy thinks about its formulary. Nothing reaches the customer that has not been checked, dated, and owned by a named person. When the formulary changes on Friday, the dispensing rules change with it. The same discipline applies to insurance voice automation. Each answer source has an owner. Each high-risk topic has an escalation rule. Each update has a review path. If a policy clause changes on Friday, the AI should not keep using Thursday's language through the weekend.

Before launch, run a knowledge gap review with 100 recent conversations. Mark each one as answerable, partially answerable, or must-escalate. If fewer than 70 are answerable from approved sources, do not launch full automation. Launch a narrower workflow instead. It is better to automate 3 call reasons safely than 12 call reasons badly.

A technical walkthrough is most useful once you have mapped deployment, knowledge, and handoff requirements; if those requirements match your insurance call center automation roadmap, book a demo with the team that will actually review the workflow.

How Revve Supports Regulated Customer Operations On Prem

Revve supports customer operations in one shared workspace rather than as a separate voice bot. Voice, chat, SMS, email, and outbound workflows share the same operating layer. For regulated teams, Revve can run in cloud or on-premise, depending on the workload and infrastructure requirements.

One runtime for AI and human agents

Revve is not a chatbot, a dialer, or a helpdesk in isolation. It is the runtime where AI agents and human agents work on the same customer conversations. That means an inbound call, a follow-up SMS, and a human escalation can stay attached to one customer thread instead of breaking across tools.

Revve's Unified AI and Human Workspace gives agents the full history when automation steps aside. The AI Voice Agent can handle inbound calls, outbound campaigns, and follow-up using configured language and conversation logic. Smart Escalation and Full-Context Handoff passes the thread, summary, prior history, and suggested next steps to a human when the workflow reaches a trigger.

That handoff matters because regulated customer conversations often include exceptions. A routine request may stay automated until the situation becomes more complex or sensitive. Revve does not remove humans from those moments. It keeps repetitive work with AI and gives judgment-heavy work to people with context intact.

Deployment flexibility for regulated teams

Revve supports cloud and on-premise deployment models. Regulated environments can use on-premise when infrastructure policy or data residency requires it. Other teams can run cloud. Same product, different deployment path.

Revve's Compliance Controls and Approval Workflows also matter here. Teams can configure consent checks, local time windows, opt-out handling, and approval steps before outbound or sensitive messages go out. Revve's Knowledge-Grounded AI Automation keeps answers tied to uploaded documents, crawled sites, and curated FAQs, rather than letting the AI speak freely on topics it has not been approved to handle.

Make Insurance Voice Automation Safe Enough To Ship

Insurance voice automation becomes safe enough to ship when it narrows scope, proves control, and keeps humans in the loop. The goal is not to automate every call. The goal is to automate the right calls, under the right deployment model, with enough evidence for operations, security, and compliance to trust it.

Pick the first workflow by risk, not volume

The highest-volume workflow is not always the best first workflow. A claim dispute may generate many calls, and it may also require empathy, document review, and exception handling. A payment reminder or claim status check may be a safer first target because the knowledge boundaries are clearer.

Use a simple scoring method. Give each workflow 1 to 5 points for volume, answer consistency, compliance risk, handoff need, and data sensitivity. Start with workflows that score high on volume and answer consistency, but low on judgment and sensitivity. That usually creates a first release that proves the system without overloading governance.

Small teams should be honest here. If you run under 20 seats or fewer than 5,000 contacts per month, the economics may not pay back yet. A human team can be cheaper at that volume. Revve is built for teams running thousands of conversations per week, where tool consolidation and automation capacity actually matter.

Ship with a human escape path

Every production AI call flow needs an escape path. Not because AI is weak, but because insurance is full of exceptions. People lose documents, miss payments, dispute claim outcomes, change addresses, and call in emotional states. A system that cannot step aside cleanly is not ready.

The release checklist should be boring:

- Define which intents AI can handle.

- Define which intents must escalate immediately.

- Set escalation triggers for negative sentiment, unresolved intent, keywords, duration, and customer tier.

- Confirm that the human agent receives the full thread and summary.

- Review 100 completed conversations before adding more workflows.

That last step is where teams learn. Not from dashboards alone, but from real calls where customers interrupt, switch language, ask unclear questions, or bring up something the script did not expect. Insurance call center automation gets better when the feedback loop is inside the operating workflow, not trapped in a spreadsheet after the fact.

The future of insurance customer operations will not be won by the vendor with the flashiest voice demo. It will be won by the team that can run voice, outbound, compliance, knowledge, and human handoff as one controlled system. For SEA BFSI, that means local-language voice, on-premise where required, and a vendor willing to meet the infrastructure reality instead of pretending every insurer can run the same cloud playbook.